Feeling overwhelmed by a mountain of debt in Dallas? Look no further than AAA Debt Solutions, specializing in debt settlement in Dallas. Our expert team is here to help you effectively handle your debt and get your finances back on track. Debt settlement has emerged as a popular solution for managing overwhelming debt and for a good reason. But what exactly is debt settlement, and why should you choose professional services? In this article, we’ll walk you through the ins and outs of debt settlement, highlight the benefits of relying on experienced professionals like AAA Debt Solutions, and showcase the advantages of utilizing our services.

Navigating the complexities of debt settlement can be overwhelming, but with the guidance of the knowledgeable experts at AAA Debt Solutions, you’ll find it much more manageable. Our team will handle negotiations with your creditors on your behalf, working diligently to reach a mutually beneficial agreement. By leveraging our expertise, you’ll save both time and money, allowing you to escape debt quicker compared to attempting to tackle it alone. Discover the numerous advantages of our expert debt settlement services that can bring you closer to financial freedom.

When you’re buried in debt, turn to AAA Debt Solutions for reliable and effective debt settlement solutions in Dallas. Contact us today to learn more about how our professional services can benefit you and help you overcome your financial challenges. Don’t let debt hold you back any longer – take control of your financial future with AAA Debt Solutions.

What Is Debt Settlement?

Debt settlement is a process by which debtors and creditors negotiate with one another to resolve the debtor’s outstanding debt. This negotiation may be done through a debt settlement company, such as AAA Debt Solutions, in Dallas, Texas, that works with both parties to come to an agreement that works for everyone involved. The purpose of this agreement is to reduce the amount of the overall debt and sometimes even eliminate it altogether. This can benefit both parties as it allows the creditor to receive some payment on the outstanding balance and provides relief for the debtor by reducing their overall financial burden.

The process of debt settlement typically begins with a consultation between the debtor and a representative from a debt settlement company or firm. During this consultation, the representative will review all of the debtor’s financial information to determine what arrangement should be made. Once this has been determined, negotiations will begin between the creditor and the representatives from an organization in Dallas specializing in debt settlement, like AAA Debt Solutions. During these negotiations, both parties will look at different options that can help them reach an agreement without further damaging either party’s credit score.

Finally, if an agreement is reached, both parties must sign off on it and follow through with whatever plan was set forth. This could include smaller payments over time or lump sum payments upfront. Ultimately, working with experts like those at AAA Debt Solutions can provide relief to those struggling with unmanageable debt while helping creditors receive some payment on their investment.

Advantages Of Settling Your Debts

Debt settlement is a great way to help you become debt free. It offers several advantages over other debt relief methods, such as bankruptcy and credit counseling. Firstly, it can help you save a lot of money. Debt settlement professionals can often significantly reduce the amount of money owed by negotiating with creditors and lenders. This means that instead of paying off the full balance owed, you could pay only a fraction of what is actually owed.

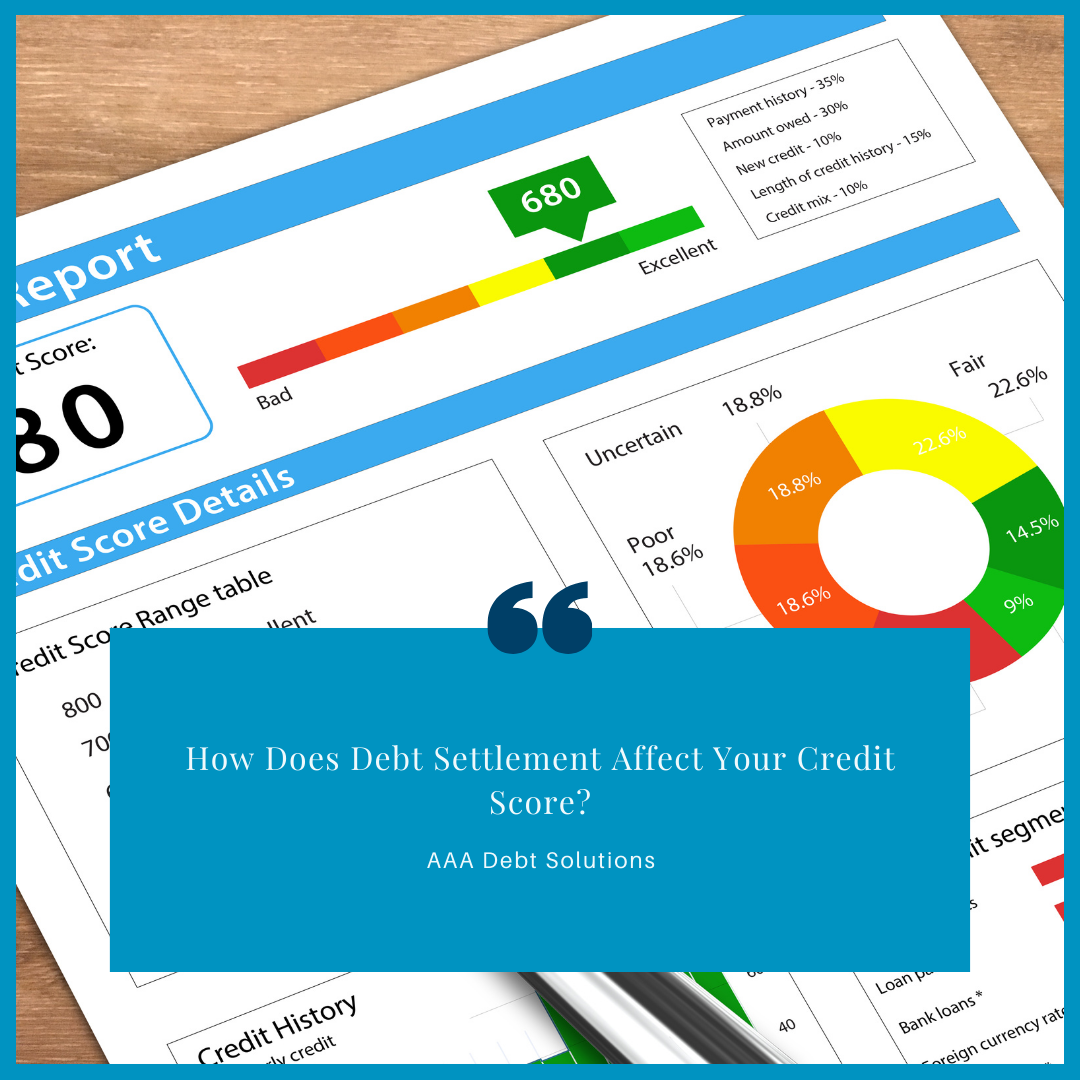

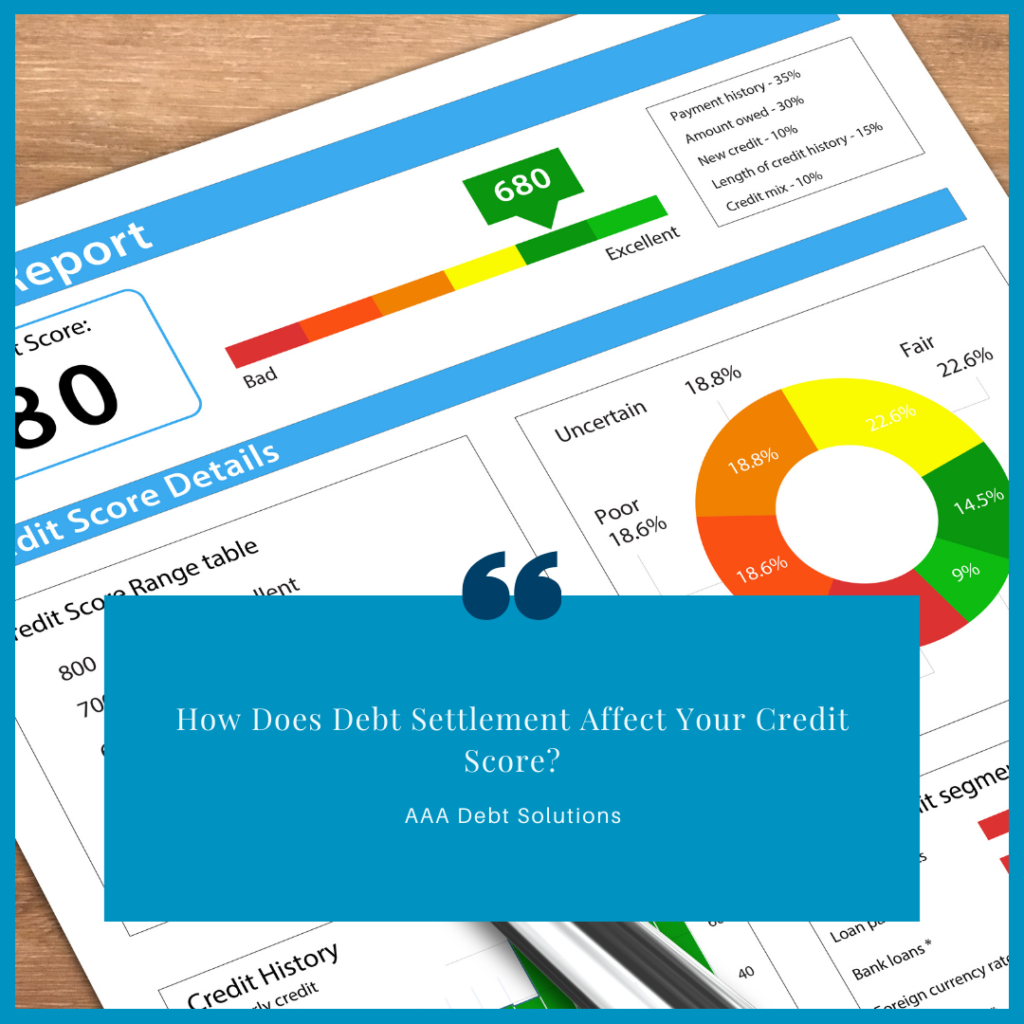

Secondly, settling debts can also improve your credit score. Since the amount owed will be reduced, this will help decrease your overall debt-to-income ratio and make it easier for you to pay off other debts faster. It also allows you to avoid damaging your credit score by filing for bankruptcy or participating in a debt management program.

Finally, by using an experienced debt settlement company like AAA Debt Solutions, you will have better chances of getting creditors to agree to settle for less than what is actually owed. With their knowledge and experience in dealing with creditors, they can negotiate on your behalf for more favorable terms and lower payments than what would otherwise be available to you if attempting the process on your own. Expert assistance may be particularly beneficial if the amount of debt is large or multiple creditors are involved.

How Debt Settlement Companies Help

Debt settlement companies can provide numerous benefits to those struggling with a large amount of debt. They can negotiate with creditors on the debtor’s behalf, helping to reduce the total owed and potentially eliminate late fees and other penalties associated with the debt. This may often be done by reducing the principal balance of the debt in exchange for a lump sum payment that is less than what was originally owed.

Debt settlement companies also specialize in helping individuals create manageable repayment plans that fit their budgets and lifestyle. These plans are created after analyzing the debtor’s financial situation and in consultation with their creditors. The goal is to find a solution that allows them to pay off their debts while still being able to maintain their current living expenses.

Finally, professional debt settlement experts can help those dealing with collections or facing legal action related to unpaid debts. They can explain available options, such as negotiating a payment plan or filing for bankruptcy if necessary, and provide guidance throughout this process. Professional debt settlement services offer valuable assistance in finding solutions that work best for each individual’s unique circumstances.

Identifying The Right Debt Settlement Company

When it comes to debt settlement, finding the right company is paramount. Knowing which companies are reputable and trustworthy can help ensure your financial goals are reached and your finances remain secure. Here are some tips for identifying the right debt settlement company.

First, research consumer review websites and contact the Better Business Bureau (BBB) to get an idea of how a company operates. Reviews from real customers can provide insight into a company’s efficiency, customer service, and overall satisfaction with its services. Additionally, the BBB can provide insight into a company’s track record and any customer complaints or reports of unethical business practices.

Second, consider the types of services offered by the debt settlement companies you’re considering. Finding a company that provides comprehensive services tailored to your needs is essential. Does the company offer one-on-one counseling? Do they have an online portal where you can manage your accounts? Are there additional resources available such as budgeting advice or credit repair assistance? These are all important considerations when choosing a debt settlement provider.

Finally, ensure you understand all fees associated with working with a particular debt settlement provider before signing up for their services. Fees should be clearly outlined in any contract and reasonable for the services provided. There should never be any upfront fees. Ask questions if anything isn’t clear or you have concerns about fees or terms of service. Ultimately, finding the right debt settlement company is essential for protecting yourself financially and reaching your goals.

Understanding The Process Of Debt Settlement

Debt settlement is a process that allows you to negotiate with creditors to reduce your total amount of debt. It involves hiring an expert who will work on your behalf to reduce the amount of debt you owe. This professional will help you identify which debts can be negotiated and how much might be reduced. They can also work with creditors to negotiate payment plans and interest rates that are more favorable for you.

The first step in the debt settlement process is to review your financial situation and determine how much debt you have and what type of debt it is. Once this information is gathered, the expert can negotiate a settlement amount with the creditors. During this process, they will discuss payment plans, interest rates, and other terms that could benefit you financially. The goal is to reach an agreement that both parties are satisfied with.

Once an agreement is reached, it must be signed by both parties before it can take effect. Once this has occurred, the creditor will stop making demands for payments until the agreed-upon amount has been paid in full. At this point, the debt will be considered settled and appear on your credit report as such. From here, you should make sure to stay current on any future payments.

Benefits Of Working With A Debt Settlement Company

By enlisting the help of a qualified professional, you can save time and money while achieving your financial goals. Here are some of the advantages that come with working with a debt settlement expert.

First and foremost, a debt settlement professional will have access to legal expertise and resources that you may not be able to access as an individual. An expert will be familiar with the debt and credit management laws and have the resources necessary to negotiate on your behalf. They will be able to identify any potential issues or loopholes in contracts that could benefit you financially. Additionally, they can advise on how best to manage your finances going forward so that you don’t end up in this situation again.

Another key benefit of working with a settlement expert is that they can help protect your credit score from further damage. When negotiating terms with creditors, they understand how best to protect your credit score so that it doesn’t take too much of a hit during the process. This is important because it allows you to rebuild quickly after settling your debts so you can start fresh financially.

Finally, when working with a debt settlement professional, they can provide guidance throughout the entire process. From helping you create a budget and develop strategies for paying off what is owed to negotiating the best deal possible on settlements — they can help guide you every step of the way until all debts are repaid in full or settled satisfactorily.

With their experience and resources, enlisting help from a debt settlement company is one of the most effective ways to ensure that all debts are paid off efficiently without taking too big of a hit on your credit score.

Pros And Cons Of Hiring A Debt Negotiator

The pros of hiring a debt negotiator are numerous. Most importantly, they can help you to reduce your total debt amount and interest rates. This can be beneficial in the long run, as it will reduce the amount of money you have to pay back over time. A debt negotiator is also able to negotiate with creditors on your behalf. This means they can work out payment plans, lower interest rates, or even get creditors to stop calling you altogether.

On the other hand, there are also some drawbacks to using a debt negotiator. For one thing, they typically charge substantial fees for their services. Depending on how much money you owe, these fees could add up quickly and offset any savings you may have achieved through their negotiations with creditors. In addition, some debt negotiators do not always have your best interests at heart; instead, they might try to convince you that their plan is the only way out of your debt problem when other options are available.

It is important that before deciding whether or not to hire a debt negotiator, you research their background and reputation carefully. Make sure they have experience working with people in similar financial situations and read reviews from others who’ve used their services. Ultimately, it is up to you whether or not hiring a debt negotiator suits you and your situation.

The Role Of A Debt Negotiator In The Settlement Process

Debt negotiation is a process that can benefit those dealing with debt. A debt negotiator is a professional who negotiates on behalf of the borrower to reduce their debt and make it easier to pay off. The negotiator will work with creditors and debt collectors to reach an agreement that reduces the amount owed, lowers interest rates, or both. This can help borrowers save thousands of dollars and get out of debt faster.

The negotiator will take into account the borrower’s financial situation and look for ways to reduce the amount owed without compromising their credit score. They’ll also negotiate with creditors on terms such as payment plans, interest rate reductions, late fee waivers, and other solutions that may help make payments more manageable. Debt negotiators are knowledgeable about laws related to debt collection, so they can protect borrowers from unfair practices or harassment by creditors.

Negotiators also provide support during the entire settlement process and ensure that everything goes as smoothly as possible. They’ll keep track of paperwork, answer any questions, and ensure your creditors are honoring their end of the bargain. With an expert negotiator helping you through the process, you can rest assured knowing that your debts are being settled in a way that works best for you. AAA Debt Solutions has a team specializing in negotiation to help with debt settlement with favorable terms.

How To Make Sure You Get The Best Deal In A Settlement

When it comes to debt settlement, getting the best deal for yourself is essential in ensuring that your financial future is well-protected. An experienced debt negotiator can help you achieve this goal. Here are a few tips on how to make sure you get the best deal when negotiating with creditors:

First, research and learn about the company’s repayment terms and policies. Knowing how much money your creditor will accept as a settlement offer and what fees may be associated with the arrangement can help you decide which option is right for you.

Second, don’t hesitate to ask questions and negotiate if necessary. Negotiations between creditors and debtors can be complicated, so it’s essential to understand all of the details before agreeing to any terms. You should also be sure to get everything in writing so there’s no confusion.

Finally, make sure you have an experienced professional working on your behalf. A qualified debt negotiator can provide valuable advice and assistance throughout the process, helping you make smart decisions that protect your financial interests now and into the future.

Avoiding Unethical Practices In Debt Negotiation

Debt settlement professionals should be held to a high ethical standard when negotiating with creditors. This is important not only for their benefit and reputation but also for the benefit of clients. To ensure this, debt settlement companies must remain aware of any unethical practices that creditors or debt collectors may use and take steps to avoid them.

One such unethical practice is using false promises and exaggerated claims to convince clients to agree to certain terms. Debt settlement professionals should always provide their clients with accurate information about the process and any potential results. They should also ensure their clients understand all aspects of the agreement before signing it.

Another unethical practice is using high-pressure tactics, such as threatening legal action against clients if they do not accept a certain offer or payment plan. Debt settlement professionals should protect their clients from these tactics, either by explaining why they are inappropriate or refusing to engage in them altogether. Debt settlement professionals must maintain an ethical stance when dealing with creditors to best serve their clients’ interests.

The most successful debt negotiation strategies are based on honesty and open communication between the parties involved rather than deceptive tactics or threats. By taking these steps, debt settlement professionals can help ensure that their clients get the best possible outcome while avoiding unethical practices.

Understanding Legal Implications Of Settlements

Knowledge about the potential legal implications of debt settlements is integral to any successful negotiation. As such, debtors must understand the laws that govern their particular situation. Fortunately, working with debt settlement companies can help ensure that all legal ramifications are considered when negotiating settlements.

In most cases, creditors are legally obligated to inform debtors of certain rights and obligations before entering into a settlement agreement. This includes providing information on how the creditor intends to report the settlement to credit bureaus and other agencies. Debt settlement experts can help ensure this process is appropriately followed, helping protect the debtor’s interests in the long term.

When settling debts, it’s important to consider tax consequences and other potential legal implications. The IRS may classify forgiven debts as income and require taxes to be paid, which could significantly impact a person’s finances. To ensure that all possible scenarios are accounted for, debtors should work with an experienced professional who understands all applicable laws and regulations. This way, they can rest assured knowing their financial future is secure and protected from surprises.

Tips For Successful Settlements With Creditors

When settling your debt, it’s crucial to have a plan. With the help of debt settlement companies like AAA Debt Solutions in Dallas, TX, you can create a strategy that allows you to pay off your creditors in a way that works for you and them. Here are some tips for successful settlements with creditors.

Start by negotiating with each creditor separately. Creditors are often willing to work with you if they know you’re serious about paying off your debt. Explain your financial situation and why it’s difficult for you to meet their demands. Offer what payment terms you can afford – such as reduced payments or an extended repayment plan – and be honest about how much money you can realistically afford to pay each month.

It’s also important to document all negotiations in writing, including the agreed-upon terms and payment amount. This will help ensure that both parties are clear on the arrangement and that all payments are made on time. Additionally, make sure any settlement agreement includes language stating that upon repayment of the debt, the creditor will delete any negative information from your credit report related to the account.

By taking these steps, you can be confident that both parties will benefit from the agreement when working towards a successful debt settlement with a creditor.

An Overview Of AAA Debt Solutions’ Services

AAA Debt Solutions is an experienced debt settlement company providing financial relief to individuals for years. They specialize in helping people consolidate debt, negotiate lower payments and develop a plan to become debt free. Their expertise can help reduce or eliminate your credit card, medical, or other consumer debts.

AAA Debt Solutions’ team of experts will create a customized solution tailored to your financial needs and goals. They offer free consultations and provide a detailed breakdown of the costs associated with their services so you know exactly what to expect. Their team of certified counselors will work closely with you to evaluate your situation and develop a plan that best fits your budget.

From creating payment plans to negotiating lower interest rates or settling unsecured debts with creditors, AAA Debt Solutions can help you get out of debt quickly and efficiently. They have helped a lot of people achieve their financial goals by providing them with personalized solutions tailored to their specific needs. They also provide educational resources to assist clients in improving their overall financial literacy so they can make informed decisions about their finances in the future.

Finding Good Reputable Companies For Debt Settlement In Dallas

Finding good, reputable debt settlement companies in Dallas can be a daunting task. It’s essential to research and ensure you’re dealing with an experienced and trustworthy company. The first step is to look for reviews online from past customers. Check if any complaints are filed against them, and find out what services they offer. You should also check their fees, as some companies may charge high fees that could cause financial hardship in the future.

Second, contact the Better Business Bureau (BBB) to see if any complaints have been filed against the company. If there are complaints, it’s best to avoid doing business with that company or at least be aware of what potential problems could arise. Additionally, ask around your network to see if anyone has had experience working with debt settlement companies in Dallas before. This can give you valuable firsthand information on reliable and trustworthy companies.

When choosing a debt settlement company in Dallas, AAA Debt Solutions encourages you to take the next important step: have a direct conversation with our knowledgeable representatives. We understand that you have questions and concerns. We are here to provide clear answers and comprehensive information about our payment plans and services.

During your conversation with our team, we will take the time to address your inquiries and ensure that you thoroughly understand how our debt settlement services in Dallas operate. We won’t rush through the conversation because we value your trust and want you to make an informed decision. By speaking directly with our representatives, you will gain valuable insights into what AAA Debt Solutions offers and how we can tailor our services to meet your specific needs. Our transparent approach and commitment to excellent customer service set us apart from the competition. You will also be able to check for the online customer reviews that testify our customers are satisfied and have benefitted from our services. We want you to feel confident and empowered in choosing a debt settlement company in Dallas.

Managing Finances After Reaching An Agreement

Ultimately, working with an expert debt settlement company can help you take back control of your finances. After reaching an agreement, it’s important to manage your finances responsibly and make all payments on time. This will help ensure that the agreement stays in place and that you remain debt-free.

First, create a budget based on your income and expenses. Knowing how much money you have coming in each month and how much is going out can help you allocate funds for essential expenses and set aside money for savings or other financial goals. Additionally, if there are any unexpected expenses, try to reduce non-essential spending first before tapping into any savings or borrowing money again.

It’s also essential to monitor your credit score after a debt settlement agreement. Continue making all payments on time, as this will improve your credit score over time and make it easier to access better financing options when needed. Finally, if you find yourself struggling financially in the future, don’t hesitate to reach out to the same debt settlement company for assistance again.

Conclusion

Debt settlement is an essential tool for those struggling with their finances. It can provide the financial freedom that so many are seeking and help to get back on track. Working with a reputable debt settlement company or expert can make the process easier, ensure better results, and provide peace of mind.

When it comes to debt settlement in Dallas, AAA Debt Solutions is a reliable company you can trust to guide you through the process successfully. Understanding the intricacies of debt settlement and finding a reputable partner like us are essential steps toward achieving financial freedom. With our expert guidance, you can organize your finances and take control of your future after reaching a settlement agreement.

Debt settlement is a serious endeavor that requires careful consideration. However, if you find yourself overwhelmed by debt, it presents an opportunity for a fresh start. At AAA Debt Solutions, our team of experts is dedicated to providing you with the necessary support and knowledge to make informed decisions that will benefit your long-term financial well-being.

By collaborating with our debt specialists, you gain access to valuable information and resources tailored to your situation. We will equip you with the tools you need to navigate the debt settlement process effectively. Our goal is to help you break free from the burden of debt and empower you to regain control over your financial future.

Choose AAA Debt Solutions as your trusted partner in debt settlement in Dallas. With our expertise and personalized guidance, you can confidently embark on your journey toward financial recovery. Contact AAA Debt Solutions at 844-844-1909 to learn more about how we can assist you in achieving a successful debt settlement in Dallas.